The Implications of Asymmetric Information in Financial Markets

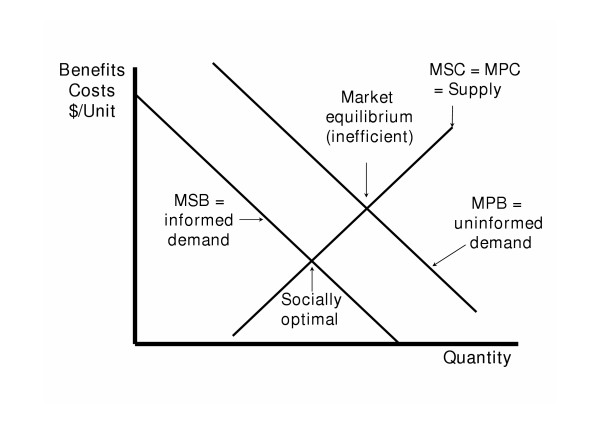

Market Equilibrium with Symmetric vs. Asymmetric Information

Asymmetric information is a key idea in information economics, suggesting that participants in the market don’t always have the same amount of information when making deals (Akerlof, 1970; Stiglitz, 2000). This isn’t just a theoretical idea; it helps us see how real financial markets differ from an idealized scenario called the Arrow-Debreu paradigm. In this ideal market, everyone knows everything there is to know, leading to perfect efficiency (Arrow, 1951; Debreu, 1959). However, in reality, the uneven distribution of information can twist market behaviors and create inefficiencies. This has significant effects on things like asset values, business finance decisions, and guidance on economic policy (Leland and Pyle, 1977; Myers and Majluf, 1984; Holmström and Tirole, 1997).

In financial markets, two archetypical manifestations of asymmetric information are adverse selection and moral hazard. Adverse selection occurs before a transaction is consummated when one party leverages undisclosed information to gain a transactional edge (Akerlof, 1970). For example, consider the market for “lemons,” used cars with undisclosed defects. Sellers have private information about the quality of the cars they sell, and buyers are unable to perfectly ascertain this quality ex-ante. This results in a market failure where high-quality cars are undervalued, and low-quality cars are overrepresented (Akerlof, 1970). Moral hazard, on the other hand, is a post-transactional phenomenon whereby one party engages in hidden actions that alter the risk profile of an asset or contract (Holmström, 1979). For instance, a borrower might take on excessive risks after obtaining a loan, knowing that the lender bears the downside.

From a mechanism design perspective, asymmetric information necessitates intricate contracts and signaling devices to align incentives and pareto-improve market outcomes (Spence, 1973; Rothschild and Stiglitz, 1976). For example, in debt markets, collateral requirements and covenants are introduced to mitigate the risk of moral hazard and adverse selection (Williamson, 1988; Hart and Moore, 1994). Similarly, in equity markets, firms employ costly signaling, such as dividend payments or share buybacks, to reveal private information and separate themselves from lower-quality counterparts (Bhattacharya, 1979; Miller and Modigliani, 1961).

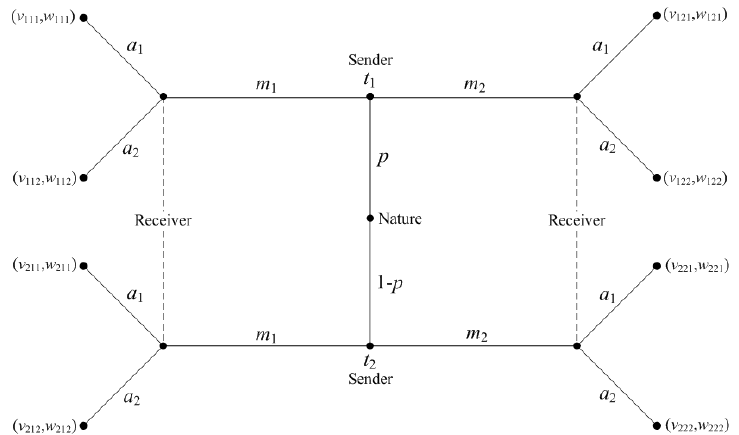

The Strategic Nature of Information Asymmetry and Game Theoretic Approaches

Signaling Game Tree, a Common Visualization of Asymmetric Information

Due to the intricate nature of asymmetric information, game theory becomes crucial for simulating how agents strategically interact. Two notable models are signaling games (Spence, 1973) and screening games (Rothschild and Stiglitz, 1976). In these models, agents either use or gather information strategically to reach a balanced outcome. Central to these games are the ideas of credibility, common knowledge, and the Bayes-Nash equilibrium. The Bayes-Nash equilibrium refers to a situation where each player’s strategy is optimal, considering the strategies of others and the probability distribution over uncertain factors. These models offer a comprehensive method to understand the issues arising from uneven information access (Harsanyi, 1967–68; Aumann, 1976).

Signaling games focus on actions taken by the informed party to credibly convey their type to an uninformed counterparty. A classic example is the job-market signaling model by Spence (1973), where education serves as a signal of productivity. In the realm of corporate finance, initial public offerings (IPOs) often underprice shares as a signal of firm quality (Welch, 1989; Allen and Faulhaber, 1989). Screening games, conversely, place the uninformed party in the driver’s seat, devising tests or mechanisms to induce self-selection by the informed party (Rothschild and Stiglitz, 1976; Riley, 2001).

In a similar way, the principal-agent model looks at issues like moral hazard in systems with levels of authority, especially in areas like executive pay and how companies are run (Jensen and Meckling, 1976; Holmström and Milgrom, 1991). When we add dynamic changes to these models, we can think about the long-term effects and how reputations are built over time, showing how financial relationships can evolve (Kreps and Wilson, 1982; Fudenberg and Levine, 1989).

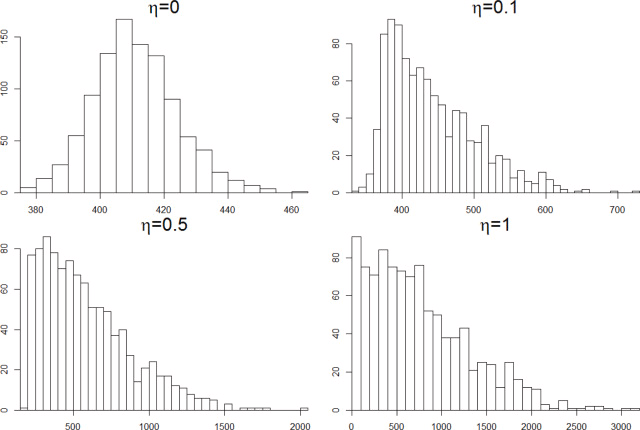

Asymmetric Information in Behavioral Finance and Market Microstructure

Distribution of Trading Volume Under Asymmetric Information

The inclusion of behavioral elements adds another layer of complexity to the asymmetric information paradigm. Behavioral finance scholars argue that cognitive biases can exacerbate the adverse effects of asymmetric information by affecting how agents process and act upon information (Shleifer, 2000; Barberis and Thaler, 2003). For example, overconfidence can make market participants underestimate the extent of information asymmetry, leading to suboptimal trading strategies and asset mispricing (Odean, 1998; Gervais and Odean, 2001).

Market microstructure literature, particularly the study of how specific trading mechanisms affect price formation, adds further nuance to the implications of asymmetric information (Kyle, 1985; Glosten and Milgrom, 1985). Market makers, who facilitate trading by quoting bid and ask prices, face the risk of “adverse selection,” wherein better-informed traders can exploit their informational advantage (Kyle, 1985; Easley and O’Hara, 1992). The issue is further accentuated with the advent of high-frequency trading, where ultra-fast trading algorithms can magnify the implications of asymmetric information (Hendershott, Jones, and Menkveld, 2011).

Conclusion

Asymmetric information remains a cornerstone concept in the edifice of financial economics. It provides the intellectual scaffolding for understanding market imperfections, from adverse selection in asset markets to moral hazard in credit markets. As this exegesis elucidates, the tendrils of asymmetric information extend into various sub-disciplines, including behavioral finance and market microstructure. The theoretical frameworks of signaling games, screening games, and principal-agent models offer elegant yet complex tools for analyzing the strategic interactions underpinning this phenomenon.

In summary, asymmetric information not only challenges the neoclassical tenets of market efficiency but also enriches our understanding by introducing realistic complexities. It accentuates the need for sophisticated contracts, regulations, and trading mechanisms to attenuate its distortive effects. While the subject continues to evolve with ongoing empirical research and computational advancements, its foundational importance in the lexicon of financial economics remains indisputable. Future research endeavors are expected to further refine these models and offer actionable insights for practitioners, policymakers, and academics alike.

References

Akerlof, G. A. (1970). The market for ‘lemons’: Quality uncertainty and the market mechanism. Quarterly Journal of Economics, 84(3), 488-500.

Allen, F., & Faulhaber, G. R. (1989). Signaling by underpricing in the IPO market. Journal of Financial Economics, 23(2), 303-323.

Arrow, K. J. (1951). Social Choice and Individual Values. Yale University Press.

Aumann, R. J. (1976). Agreeing to disagree. The Annals of Statistics, 1236-1239.

Barberis, N., & Thaler, R. (2003). A survey of behavioral finance. Handbook of the Economics of Finance, 1, 1053-1128.

Bhattacharya, S. (1979). Imperfect information, dividend policy, and ‘the bird in the hand’ fallacy. The Bell Journal of Economics, 259-270.

Debreu, G. (1959). Theory of Value: An Axiomatic Analysis of Economic Equilibrium. Yale University Press.

Easley, D., & O’Hara, M. (1992). Time and the process of security price adjustment. The Journal of Finance, 47(2), 577-605.

Fudenberg, D., & Levine, D. K. (1989). Reputation and equilibrium selection in games with a patient player. Econometrica: Journal of the Econometric Society, 759-778.

Gervais, S., & Odean, T. (2001). Learning to be overconfident. The Review of Financial Studies, 14(1), 1-27.

Glosten, L. R., & Milgrom, P. R. (1985). Bid, ask and transaction prices in a specialist market with heterogeneously informed traders. Journal of Financial Economics, 14(1), 71-100.

Hart, O., & Moore, J. (1994). A theory of debt based on the inalienability of human capital. The Quarterly Journal of Economics, 109(4), 841-879.

Harsanyi, J. C. (1967–68). Games with incomplete information played by ‘Bayesian’ players, I–III. Management Science, 14, 159-182, 320-334, 486-502.

Hendershott, T., Jones, C. M., & Menkveld, A. J. (2011). Does algorithmic trading improve liquidity?. The Journal of Finance, 66(1), 1-33.

Holmström, B. (1979). Moral hazard and observability. The Bell Journal of Economics, 74-91.

Holmström, B., & Milgrom, P. (1991). Multitask principal-agent analyses: Incentive contracts, asset ownership, and job design. Journal of Law, Economics, & Organization, 7, 24-52.

Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305-360.

Kreps, D. M., & Wilson, R. (1982). Reputation and imperfect information. Journal of Economic Theory, 27(2), 253-279.

Kyle, A. S. (1985). Continuous auctions and insider trading. Econometrica: Journal of the Econometric Society, 1315-1335.

Leland, H. E., & Pyle, D. H. (1977). Informational asymmetries, financial structure, and financial intermediation. The Journal of Finance, 32(2), 371-387.

Miller, M. H., & Modigliani, F. (1961). Dividend policy, growth, and the valuation of shares. The Journal of Business, 34(4), 411-433.

Myers, S. C., & Majluf, N. S. (1984). Corporate financing and investment decisions when firms have information that investors do not have. Journal of Financial Economics, 13(2), 187-221.

Odean, T. (1998). Volume, volatility, price, and profit when all traders are above average. The Journal of Finance, 53(6), 1887-1934.

Riley, J. G. (2001). Silver signals: Twenty-five years of screening and signaling. Journal of Economic Literature, 39(2), 432-478.

Rothschild, M., & Stiglitz, J. E. (1976). Equilibrium in competitive insurance markets: An essay on the economics of imperfect information. The Quarterly Journal of Economics, 90(4), 629-649.

Shleifer, A. (2000). Inefficient markets: An introduction to behavioral finance. Oxford University Press.

Spence, M. (1973). Job market signaling. The Quarterly Journal of Economics, 87(3), 355-374.

Stiglitz, J. E. (2000). The contributions of the economics of information to twentieth-century economics. The Quarterly Journal of Economics, 115(4), 1441-1478.

Welch, I. (1989). Seasoned offerings, imitation costs, and the underpricing of initial public offerings. The Journal of Finance, 44(2), 421-449.

Williamson, O. E. (1988). Corporate finance and corporate governance. The Journal of Finance, 43(3), 567-591.