From 2007-2009, the United States witnessed its biggest economic crash since the Great Depression. The Great Recession left 8.8 million people without jobs, shooting unemployment up to 10% and leaving about 10 million Americans without homes. The stock market crashed with the DOW dropping around 7,000 points or 54% in a span of 18 months. Overall, U.S. stocks lost one-third of their value. For millions of people, this meant seeing their retirement savings drop by one-third. Old financial institutions like Lehman Brothers went bankrupt and others like Bear Stearns merged with other banks. The government bailed out most of them. But the problems were not only in America. Around the world, stocks plummeted and economies collapsed. Iceland’s banking system collapsed and many European nations entered a debt crisis.

But what caused all of this? There were many factors that led to the recession, but most of it was due to the securitization of subprime mortgages into mortgage-backed securities (MBS) and collateralized debt obligations (CDO).

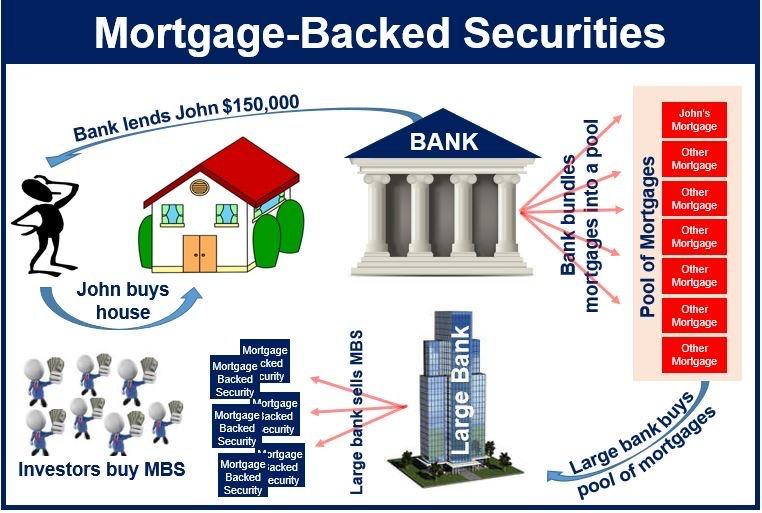

Residential Mortgage-Backed Securities

Before the 2000s, it was hard to obtain a mortgage if you had bad credit or did not have a steady job. A mortgage is a loan that people take out to buy a home. Rather than paying all the money upfront, mortgages allow them to pay for their home over a period of time. Lenders did not want to take the risk of having people default on their loans. However, in the early 2000s, investors began looking for a low-risk, high return investment. They started investing in the U.S. housing market, which they saw as extremely stable. Investors became attracted to owning parts of people’s mortgage debt which offered stable and high interest rates. Owning mortgage debt means that the owner receives the mortgage payments.

Residential and Commercial MBS

Rather than buying individual mortgages, investors bought residential mortgage-backed securities. Residential mortgage-backed securities (RMBS) are backed by homes. In contrast, commercial mortgage-backed securities (CMBS) are backed by income-generating commercial properties such as malls, office buildings, or retail centers. Large financial institutions create RMBS by securitizing mortgages. Securitization occurs when investment banks buy thousands of individual mortgages, bundle them together into one package, and sell shares of that to investors. Unlike regular commercial banks that mostly give out loans to individuals and small businesses, investment banks help sell securities, create new securities, and help to drive mergers and acquisitions.

Say we have 5 mortgages belonging to Jack, Jane, Smith, Mark, and John, each worth $200,000 each but with differing interest rates. Rather than selling all these mortgages individually, an investment bank will securitize them by buying them and then combining them into a mortgage-backed security. They then sell this mortgage-backed security as a bundle that contains $1,000,000 worth of mortgage debt with an interest rate that is the weighted average of each of the individual interest rates.

Investors bought into mortgage-backed securities as they provided a high rate of return and seemed like very safe bets because housing was so stable. As home prices were rising, investors figured the worst outcome would be that the borrower defaults on their loan and they could sell the collateral, often the house, for more money. Collateral is basically a form of protection for the banks. If borrowers default on their loan, banks can seize the collateral, which is generally an asset such as a house, and sell it to make up for the lost money. Additionally, credit agencies labeled mortgage-backed securities as safe investments, giving them AAA ratings.

Securitization of Subprime Mortgages

At first, mortgage-backed securities comprised of stable mortgages with good credit ratings. But, investors became desperate to buy more mortgage-backed securities, so lenders had to create more of them. However, the number of mortgages owned by borrowers with good credit ratings was very small. So, in order to create more mortgage-backed securities, banks needed more mortgages.

Banks began to loosen their standards for who can qualify for a mortgage. They began to make mortgage loans to people with bad credit ratings and low income. These are subprime mortgages. The lenders would then bundle up the subprime mortgages, securitize them into mortgage-backed securities, and sell them to investors. Because these mortgages were subprime, they offered even higher returns to compensate for the higher risk of default, making MBS with subprime mortgages seem even more attractive.

Some places even began applying predatory lending practices to generate more mortgages such as NINJA loans. Subprime lenders gave NINJA (No Income, No Job, and no Assets) loans without verification of income, employment, or asset ownership. Subprime lenders generally gave them to people who had poor credit scores. To make them affordable, they offered adjustable mortgage rates that would start off with a lower interest rate which then increased later on. The practice was relatively new so rating agencies gave them good ratings. Historically, mortgage debt was safe. However, as the number of subprime mortgages being created grew, they became less safe.

Collateralized Debt Obligations

At the same time, banks created and sold an even riskier product called collateralized debt obligations (CDO). Credit agencies gave CDOs high credit ratings despite having risky loans. They are a type of derivative, meaning that they derive or get their value from an underlying asset. In the case of the 2008 crisis, the underlying assets were mortgages. Additionally, the underlying asset also serves as the collateral. CDOs are a type of mortgage-backed security.

CDO Tranches

CDOs contain different tranches. Tranches are like levels, where each tranche has different amounts of return rates but also different levels of risk. The more risk an investor takes on, the higher his potential return rate. There are generally 3 different tranches; senior, mezzanine, and equity. Equity, the lowest level, has the most risk but also the highest return. As we move our way up the tranches, risk and return both decrease with Senior being the least risky while also having the lowest returns. If borrowers default on their loans, Equity and Mezzanine levels will take the hit so holders of Senior level CDOs will still get their money back. CDOs are basically mortgage-backed securities with different levels of risk and different rates of return.

Let’s say we have two investors; Joe and Jack. Joe is a low-risk type of person and is fine with low returns. On the other hand, Jack is a high-risk type of guy and is chasing huge returns. Now let’s say we have an MBS that has a rating of BBB and a return rate of 7%. Joe thinks the risk of a BBB rating is too high so he does not invest. On the other hand, Jack thinks the 7% return is too low so he also does not invest. And this is where CDOs become very appealing. CDOs offer different tranches so Joe can get a Senior tranche that is AAA rated with a 3% return rate and Jack can get an Equity tranche that is B rated with an 11% return rate.

Leading up to the crisis, investors put huge amounts of money into CDOs because they assumed the growth of the housing market, even in the lower tranches, was safe. However, when things began to turn south and the housing market began to fall, not even the people in the highest tranches were safe from the collapse.