Life is full of danger. Natural disasters, accidents, injuries, and more are all morbid topics, but they are a part of life — or death, for that matter. If we have families and close friends, chances are that at least some of them are partially or fully financially dependent on you. If you died today, what would happen next? Without a stable source of income (which normally would have come from your job/business), your loved ones face a long and arduous journey of financial hardship. What can we do about this? Life insurance can help ease this tension.

The Basics

Life insurance is a type of insurance with a contract between an insurance payer and an insurance policy holder. The payer gives money to the policyholder each month in exchange for a promise that in the event of the payer’s death, the policyholder/the represented insurance company will pay a death benefit (e.g. “reward”). However, certain events, such as fraud, riots, war, and more are not covered in this policy.

Life insurance usually has an application process. In the application, you answer questions about your health and medical conditions. Additionally, you will be subject to a medical exam to assess your physical fitness. The more fit you are, you will likely have to pay a smaller monthly fee. Insurance companies want to maximize profits, so if you are unhealthy, you become a liability to the company. For this reason, insurance companies will charge more in the hopes to recuperate any losses they may face if you pass away prematurely. Certain attributes, such as obesity, drug use, pre-existing medical conditions, diseases, or a hazardous occupation can hurt your chances of getting lower monthly fees. Age, gender, and face amount (value) are also factored into the consideration of the monthly cost of life insurance.

Term and Permanent Insurance

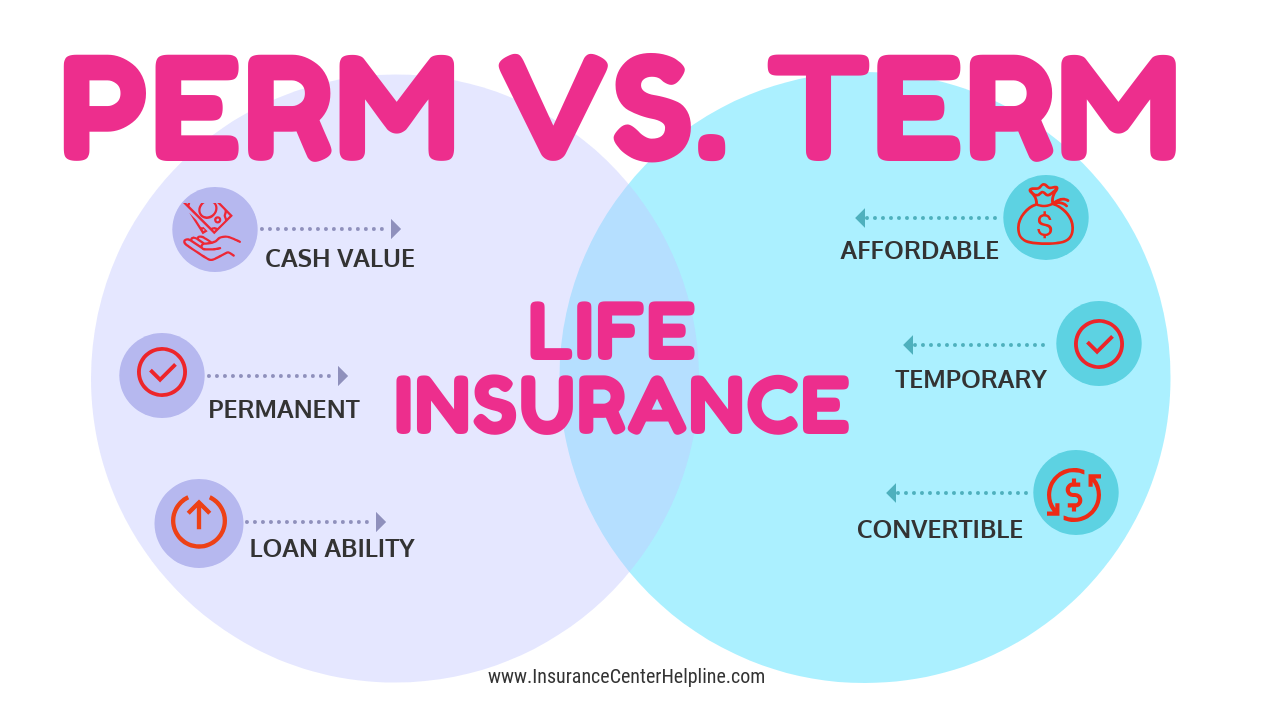

There are two types of Life Insurance: term and permanent insurance. The difference between the two is time—term life insurance lasts for a certain number of years (usually ~30), while permanent life insurance lasts until your death. There are advantages and disadvantages to both, and each can be the better choice depending on the situation.

Term life insurance protects you for a certain number of years, so it’s relatively low-commitment. Due to the contract being binding for only a few years, companies will give you better monthly rates because there is a higher chance that you will outlive your term life insurance. In addition, this can be beneficial during your high-earning and high-spending years, because in the case of your passing, your family will be able to maintain their current lifestyle.

On the other hand, we have permanent life insurance (also known as whole life insurance). The advantage of this is that your family will receive a monetary boost following your death. This is especially appealing for people in unstable financial situations. You can also purchase add-ons called “riders”, such as long-term care coverage, to improve your quality of life and care. This is exclusive to permanent life insurance.

Another feature of permanent life insurance is cash value. This is when you pay extra money on top of your monthly payment, with which the insurer invests into the stock market (i.e. S&P 500) to give you returns (or losses). If the market continues to increase, you generate more profit until you don’t even need to pay for life insurance premiums, as the investment returns cover it! Choosing term or permanent life insurance is a big decision, and if you choose right, you can greatly impact your family’s future financial stability.

X-Curve

The x-curve is an illustration that shows the relationship between responsibility and wealth as time goes on.

As shown above, your responsibility decreases while your money increases as time goes on. At a young age, you have responsibilities such as debt, family, home, car, etc. It’s also likely you haven’t advanced far in your career. But by the end of your financial life, you (ideally) would have a lot of money from your career and investments, and you would have paid off your family’s expenses and your own debts. If you pass away earlier than normal, your family will fall into a predicament, as they will be in their high spending years without any money to support them. This is where protection comes in, which guarantees death benefits in return for premiums through contracts such as term/permanent life insurance.

Term life insurance is usually used during your high-earning and spending years (before your retirement). If you’ve been managing your money well, by the time you retire, your money should be making you money! Even in Stage 2 in the picture, living longer than usual can reap benefits through permanent life insurance. As previously mentioned, longevity is compensated with riders on your perm insurance such as long-term care or chronic/critical/terminal illness riders, to increase quality of life in the “endgame”.

Conclusion

Death is a touchy subject for people. However, it’s an important topic to discuss with your loved ones. It is imperative that we pay for life insurance, as our small “investment” will pay off well in dire times. Our heirs will thank us when they have sufficient money to live comfortably and reach their goals without limitations. Everyone wins with life insurance.