The Federal Reserve, commonly dubbed as the “Fed,” is the gatekeeper of the U.S. economy. Its role is to regulate the nation’s financial institutions, such as banks, credit unions, etc. It’s always important to keep an eye on markets when it comes to the Fed meetings. The current chair is Jerome Powell. But before you listen to what he says, you must understand the roots of the Fed itself.

Origins of the Federal Reserve: The Panic of 1907

Bank failures in the past, business bankruptcies, and economic disruptions led to the Federal Reserve. More specifically, the Panic of 1907 served as the catalyst for the Fed’s creation. The trigger for this panic was a failed effort by two people — F. Augustus Heinze and Charles W. Morse — to corner the market Heinze’s company, the United Copper Company. Cornering the market is a stock manipulation scheme that aims to take control of a large amount of stock of a company. Once you own enough stock, you are able to manipulate its price.

Heinze’s Plan

Heinze’s plan was based on two assumptions. The first was that Heinze already controlled a majority of the company. The second was that a large number of shares of his company were being sold short. Learn about how shorting works by checking out this article about a famous short: Bill Ackman Versus Herbalife: What Happened. Their plan was to raise money from banks and use that money to buy and bid up the price of the company’s stock in hopes of causing the short sellers to cover their shares by buying them from the Heinzes. That is also known as a short squeeze. At that point, the Heinzes, who would control the market for those shares, could sell their shares to the short sellers for any price they wanted.

This plan failed spectacularly. Heinze did indeed bid up the price of his company’s shares, but when he called for short sellers to cover, the short sellers easily found other sources from which to buy United Copper Company’s shares cheaper than what Heinze was offering. After the massive buying, Heinze did not anticipate short-sellers finding another market for the stock. Because they found a market to buy the stock cheaper, the stock’s price collapsed. That ruined Heinze and the banks which he raised money from to finance his cornering effort.

Weakening Depositor Confidence and Bank Runs

Word of this collapse spread throughout and caused depositor confidence to drop. Depositor confidence is the trust depositors have in a bank’s abilities to pay withdrawals and interest on accounts. When depositor confidence drops, depositors often rush to withdraw their money because of a weakened belief that their banks provide safety for their money. This rush to withdraw funds from banks, also known as a bank run, caused many banks to become insolvent. Being insolvent means being unable to pay their debts. Deposit accounts are debt for banks because banks need to pay interest on those accounts. Only the banks that had lent money to Heinze closed down because the depositors who withdrew from those banks simply went to other banks.

Trust Companies

However, there was another way to store money: trust companies. Trust companies, put simply, operated like banks but with much looser regulation. One of those looser regulations manifested in the form of a smaller reserve requirement. The requirement was 5% for trust companies in the early 1900s. That is not much, which further exposed trust companies to bank runs. One such trust company, the Knickerbocker Trust Company, due to past association with Heinze and Morse, succumbed to weakening depositor confidence and a subsequent bank run.

Liquidity Crisis

This news spread, and banks and trusts became more reluctant to lend money. This meant that companies and people that rely on loans to fund their activities couldn’t do so anymore. This is what is called a liquidity crisis. Another way to think of a liquidity crisis is as a massive shortage of funding. Liquidity refers to the ease with which you can convert a certain asset to cash without losing value. The effect of the liquidity was that brokers were unable to get loans (shortage of funding) to fund stock purchasing, which caused stock prices to fall to record lows. This had a cascading effect that led to more bank runs, weakened depositor confidence, and, ultimately, a financial crisis.

Due, in large part, to the efforts of financiers like J.P. Morgan and John D. Rockefeller, as well as the government, the panic was alleviated. The aftermath of this panic raised many questions about how to deal with the financial crisis and times where liquidity and funding were in short supply. These questions were answered with the creation of the Federal Reserve, the US’s central banking system.

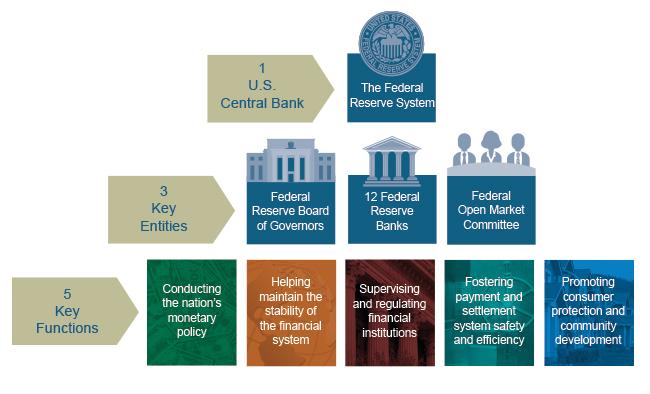

Regional Banks

The Fed is consists of 12 regional banks that are responsible for their own geographical area. These areas are based in San Francisco, Dallas, Kansas City, Minneapolis, St. Louis, Chicago, Atlanta, Richmond, Cleveland, Philadelphia, New York, and Boston. Although government officials do not directly work with the Fed, the Fed officials work with the government’s policy objectives. Everyone should learn the basics of the Fed as it is the largest influence on monetary policy.

FOMC

The Federal Reserve’s body is the Federal Open Market Committee (FOMC), which consists of multiple sections. This includes the four regional Federal Reserve Banks, New York Federal Reserve Bank president, and the Board of Governors. Officials serve these sections on a rotating basis.

This committee holds four main responsibilities for the decisions of monetary policies:

- Moderating all bank institutions to ensure customers are protected with their money

- Providing certain financial services to the U.S. government, U.S. financial institutions, and foreign official institutions, and playing a major role in operating and overseeing the nation’s payments systems

- Managing monetary policy, meaning changing the federal funds rate, which influences monetary and credit conditions across the nation

- Maintaining the stability of the financial system by containing problems that may arise in financial markets

Federal Funds Rate

The Fed is arguably the most powerful financial institution in the world as it watches over the world’s largest economy. Its main tool to manage monetary policy is the federal funds rate. The federal funds rate is the rate at which the borrowing bank pays the lending bank to get to the required minimum reserve amount. If a bank doesn’t have sufficient funds to pay withdrawals and interest for customers, the bank would have to borrow the funds to do so from another bank.

If a bank doesn’t have sufficient funds to pay withdrawals and interest for customers, the bank would have to borrow the funds to do so from another bank. Banks with more than the required minimum fund amount in their reserves can loan their funds in excess of that minimum to banks that don’t meet that requirement. The reserve requirement is a percentage of a bank’s total deposits, and it’s currently 10% for large banks. The reserve requirement ensures that banks have sufficient funds to cover withdrawals in case of an event that triggers mass withdrawals.

The Federal Reserve influences the federal funds rate by setting a target rate for it. When you hear that the Fed increased or decreased interest rates, it’s the target rate for the federal funds rate that changed. Those changes have a ripple effect on the interest rates and yields across all asset markets, especially the bond market.

A Guide to Interest Rate Hikes and Cuts

A rate hike is an increase in the target rate. A rate cut is a decrease in the target rate. Here’s a basic guide to the idea behind interest rate hikes and cuts:

- When the Fed cuts interest rates, banks loan money to each other at a lower, cheaper rate. That leads banks to issue cheaper loans, which leads to people taking out more loans. That results in those loans, of which there are more of, being used for a greater amount of spending. That spending leads to more business growth. That ultimately affects expectations of business growth and often leads to a more optimistic view that often contributes to rising stock and bond prices.

- When the Fed hikes interest rates, banks loan money to each other at a higher, more expensive rate. That leads banks to issue more expensive loans, which leads to people taking out fewer loans. That results in those loans, of which there are fewer of, being used for a smaller amount of spending. That spending leads to less business growth. That ultimately affects expectations of business growth and often leads to a more pessimistic view that often contributes to declining stock and bond prices.

Key Takeaways

- The Federal Reserve System is considered the national bank of the United States.

- The FRS gives the nation a protected, adaptable, and stable monetary and financial system.

- Referred to just as the Fed, it is involved 12 regional Federal Reserve Banks that are each liable for a particular geographic territory of the U.S.

- The Fed’s primary obligations incorporate directing monetary policy, administering and controlling banks, keeping up financial sustainability, and providing bank services.

By playing out the entirety of its different obligations—setting interest rates, supervising and regulating financial institutions, providing national payment services, and maintaining the stability of the nation’s financial system—the Fed is essential to watch out for as it assumes a pivotal job in saving the wellbeing of the economy, particularly during times of financial emergency.