There is no doubt that everyone has heard the saying that “time is money.” More than something that your parents would say in a lecture to you about not wasting money they spent hours working for, this saying derives itself from the core idea in all of finance: the time value of money. Simply said, the time value of money is the idea that an amount of money received earlier is worth more than that same amount of money received later. In other words, a dollar received today is worth more than a dollar received tomorrow. Money received earlier is worth more because the sooner you have money, the sooner you can invest that money, and the longer your investment has to grow in value.

Present and Future Value

There are two concepts and a little bit of math relating the two associated with the time value of money. The two concepts are present value (PV) and future value (FV). Present value is what it sounds like: the current value of your investment. Future value is the value of your investment at a specified time in the future. The formula to determine the FV and PV of your investment are as follows:

Where i is the interest rate in decimal form, n is the number of compounding periods per year, and t is the duration in years for the investment.

Relation to Compound Interest

If the FV formula looks familiar, that’s because it is the same as the compound interest formula. In fact, the compound interest formula derives itself from the FV formula, and the only difference is that FV becomes amount (A) and PV becomes principal (P). Principal refers to the initial amount of money put in an investment. Let’s look at some examples of how to use the time value of money, assuming only one compounding period per year (n = 1):

- What is the FV of an investment after 1 year if the PV is $2,000 and the interest rate is 5%?

- What is the PV of an investment if after 5 years your FV is $10,000 and your interest rate is 8%?

For the first example, you would use the FV formula, and just plug numbers into the formula:

FV = $2,000 x (1 + (0.05/1) )(1 x 1) = $2,000 x (1.05) = $2,100.

This means that if you find an investment growing at 5% every year and invest $2,000 in it, after 1 year your investment would be worth $2,100.

For the second example, you would use the PV formula, which is just solving for PV from the FV formula.

PV = $10,000 / (1 + (0.08/1)(5 x 1) = $10,000/(1.085) ≈ $6,805.83

This means that if you find an investment growing at 8% annually, for it to be worth $10,000 in 5 years, you would have to invest about $6,805.83 now.

TVM: The Lottery, Present, and Future Value

An interesting application of the time value of money is with the lottery. Most of us are familiar with how the lottery works: buy a ticket, possibly win the pool, and get paid that amount. However, there are two ways to get paid the lottery winnings: lump sum or annuity. Lump-sum means that the lottery winner gets the entire amount all at the same time, and is also taxed based on that amount. Annuity means that the lottery amount gets paid over time through fixed payments on a fixed schedule.

Let’s say that someone wins a lottery worth $10M. He has the option to take the $10M lump sum or through annuity with payments of $1M over ten years. Which option is better?

Lottery With Annuity

Let’s start with the annuity option. In this case, the winner gets only $1M now, and $1M a year from now, and another $1M two years from now, and so on and so forth till $10M has been paid to him. If a dollar today is worth more than a dollar tomorrow, then $1M received today is worth more than $1M received in the future. After receiving the $1M now, the winner must wait one entire year to get another $1M. Let’s say that today, the winner invests his first $1M in an investment that grows at 10% and plans on holding that investment for 10 years. That $1M will be worth $1M x (1.1)^10 ≈ 2,593,742.46 in 10 years.

After one year, the winner receives the second payment of $1M, and he puts that into the same investment he put his initial $1M in. But, since one year has passed, the winner’s second $1M has 9, not 10, years to grow. The value of that $1M at the end of the remaining 9 years is $1M x (1.1)^9 ≈ 2,357,947.69, which is less than what the initial $1M would be worth at the end of the investment. As the winner keeps getting his payments of $1M, he puts it into the same investment, but everytime he does, each $1M has less time to grow. If you see the table below, at the end of ten years, your investment is worth about $18.5M.

While $18.5M is certainly a lot of money, let’s still take a look at the lump sum option.

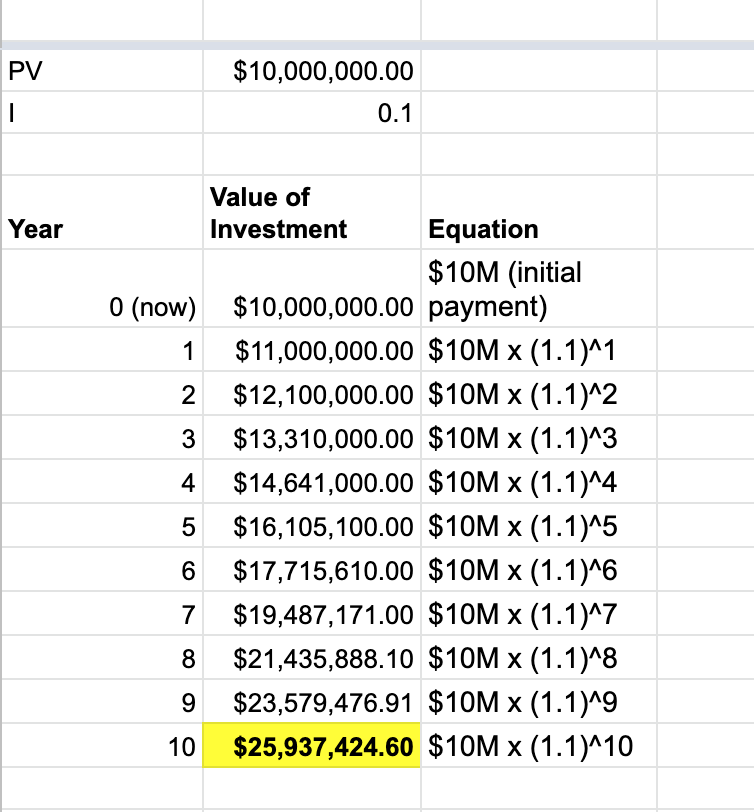

Lottery with Lump Sum

If the winner took the $10M lump sum, he would have $10M to invest. For the sake of simplicity, this example will ignore the tax on the $10M. Below is a table showing the value of the investment by year. With the lump sum option, the winner ends up with about $25.9M at the end of ten years.

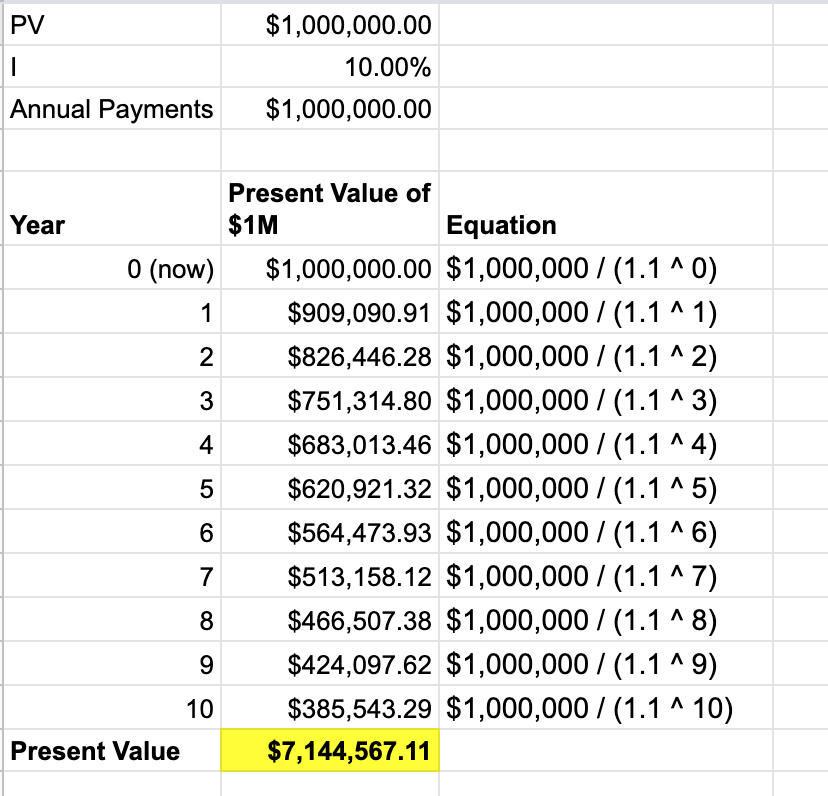

The lump sum is clearly the better option, earning about $7.4M over the 10 year investment than the annuity investment. According to the time value of money, it makes sense that the annuity option, which spreads payments over time, is worth less than the lump sum. Each $1M payment isn’t worth $1M in the present because that $1M hasn’t been growing from today. So what is the present value of $10,000,000 with the annuity option? To figure that out, the present value formula must be used to calculate the value of each one $1M, using the 10% growth rate of the investment.

The present value of the annuities is $7,144,567.11, about $2.9M less than the lump sum present value of $10M. So, if a lottery winner takes the annuity, he or she is actually getting ripped off by the lottery organizers.

Relation to Interest Rates

Imagine if your friend proposes to pay you $1,200 in five years if you loan him $1,000. If you want to earn a 3% interest rate, should you accept this deal? Well, let’s plug it into the equation: your friend is willing to pay you $1,200 in five years, so the future value is $1,200 and the “t” is equal to 5. Then if you plug 0.03 (3% interest) in for r and solve, you find the present value of the investment is $1,035.13, or more than you have to pay. Therefore this is a good deal for you. Let’s assume the compounding period is 1 (n = 1).

PV = FV / (1 + i)t = $1,200 / (1 + 0.03)5 = $1,035.13

However, say the economy is in great shape and other investments will net you a 5% interest rate. Then is this still a good deal? If you plug in 0.05 for “i” instead of 0.03, the present value comes out to be $940.23, making the deal unfavorable to you. Thus as interest rates rise and future value stays constant, the present value falls. This, in a sense, is the principle behind discounted cash flow. The present value and interest rates are indirectly proportional. What if your friend offers to pay you back the same amount in 10 years, instead of five, and you want 3% interest on your investment? Plugging those numbers into the equation spits out a present value of $892.91. Thus the number of years until maturation and the present value are also indirectly related.

PV = FV x (1 + i)t = $1,200 x (1 + 0.05)5 = $940.23

PV = FV x (1 + i)t = $1,200 x (1 + 0.03)10 = $892.91

Conclusion

The time value of money is a core principle in finance. Every investor (and lottery winner) should know about the time value of money, present value, and future value to evaluate and make strategic investments.