In a capitalist society, money is power to businesses. Institutions that generate revenue — for-profits and non-profits, corporations and single-employee businesses, farms and automobile factories alike — eventually need to achieve solvency to be sustainable long-term. The economy cycles between periodic highs and periodic lows, and as much as businesses may want to prolong periods of growth, they are all subject to the vagaries of supply and demand, federal banking practices, and other factors of a developed economy. Institutions know that keeping cash is useful in a worsening economy, but presents an opportunity cost when compared to investing that cash in the form of paying shareholders dividends, buying out competitors, and otherwise attempting to get a return on their cash. Even businesses that aren’t traditional “businesses” can do this.

Enter the world of university endowments: a place for wealthy non-profits to leverage the power of the economy, for good or for bad, and evade both taxes and loss of their non-profit status.

The History of Endowments

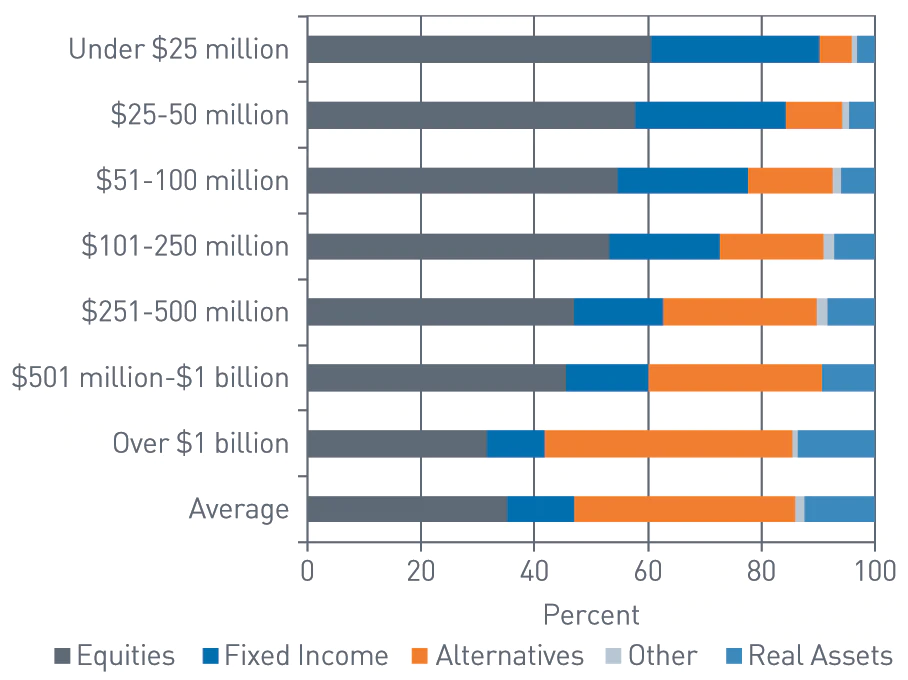

We will define an endowment here as the net value of an educational institution’s cash, security, real estate, mutual fund, and other investment assets such as non-traditional investments, like debt in foreign countries. Endowments in their present form have their genesis in the 1970s when university systems began to invest more heavily in illiquid assets like natural resources and direct commodities. Before that time those investments were concentrated in real estate. Industrial securities and railroad equities were also popular at that time.

Now, endowments’ portfolios make use of broad market securities, mostly mutual funds (and more rarely, index funds), foreign debt, commodities, fixed income, and less real estate than a century ago. These funds mostly grow through philanthropic donations by alumni and others and through returns on their principal value.

The Status of U.S. Endowments

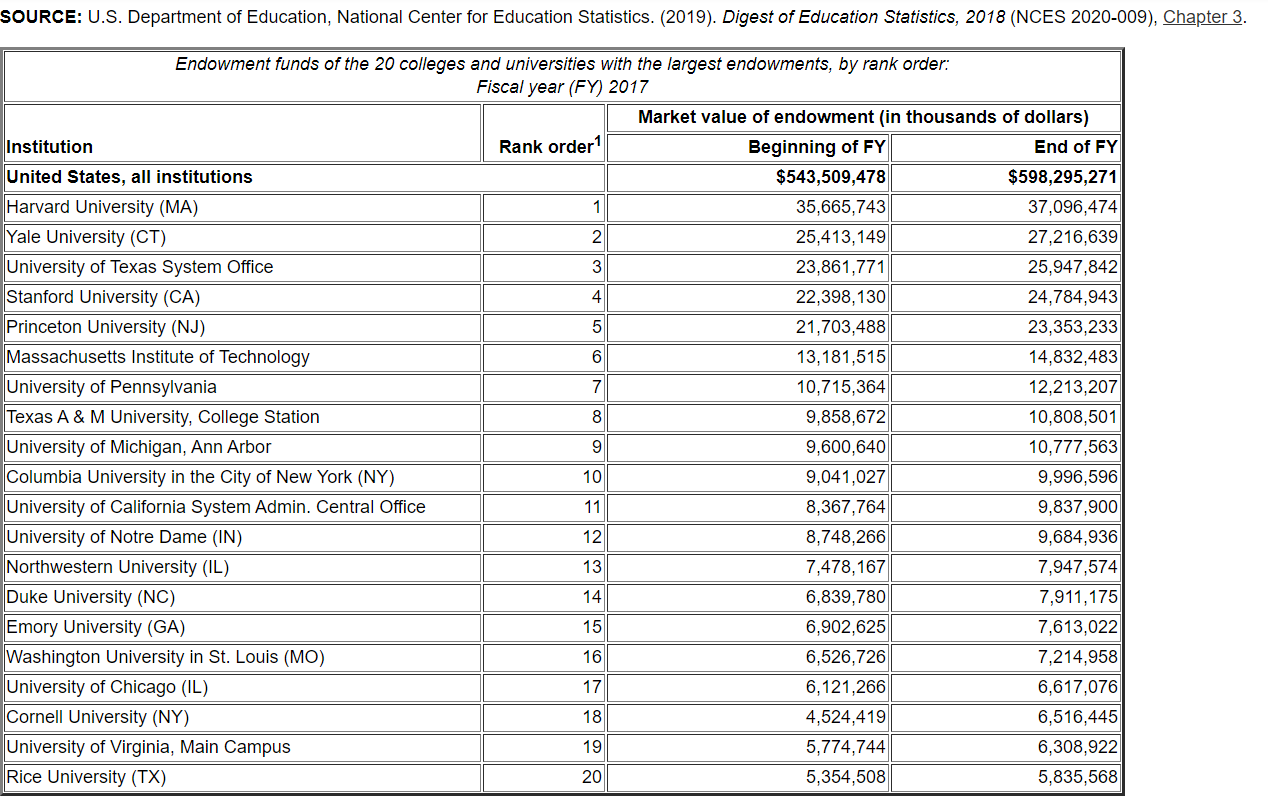

According to 2017 data from the National Center for Education Statistics, the sum of the endowment funds of all U.S. colleges and universities was nearly $600 billion, where the 120 institutions with the largest funds accounted for nearly 75% of that total. Harvard University, with an investment pool three-quarters the size of the Gates Foundation, accounts for $35 billion of that total, and the largest public university system (the University of Texas organization) accounts for $25 billion. 54% of all private universities and colleges have less than $10 million endowed to them.

From the end of fiscal year 2016 to that same time in 2017, the figure for all colleges and universities increased 10%, indicating that the average return on those endowment funds was 10%. Sounds pretty good, right? In that year, the DJIA returned 25.08%, and the S&P 500 returned 19.42%.

This means that passive total market indexes did at least twice as good as actively-managed college and university endowments did in that year. Perhaps it was just a bad year. Let’s zoom out and look at average figures. In the trailing 10-year period, college endowments have averaged a 8.4% return, the DJIA has averaged a 11.78% return, and the S&P 500 has averaged a 12.05% return, both using DQYDJ’s return calculators and economist Robert Schiller’s historical data (without dividends reinvested). Without dissecting the data any further, it’s evident that something is amiss.

Endowment Management and Withdrawals

If college and university endowments have underperformed in the past decade as compared to indices, are there any redeeming qualities that make their returns look reasonable? Well, it really depends on how you slice it. From a profitability standpoint, one can view endowments as retirement accounts for non-profit educational institutions. They generate tax-free returns and serve as lifelines in times of crisis and ill circumstances. At the same time, extremely large funds can generate huge profits for those who manage them. In 2017, Harvard Management Company paid $40.5 million to its top 5 endowment managers. Yale senior investment director David Swensen received $4.7 million for his services.

At the same time, it is a well-known fact that mutual funds (which these endowments can be related to, as they are characterized by cash inflows through donors) become increasingly difficult to manage as their assets under management pile up, which can be read more about here. The issue of scaling is often why mutual funds close their doors to new investors after a self-defined threshold is met, but it is almost against the purpose of an endowment to stop accepting donations: how can a university or college expect to insure itself against being strapped of cash by a future need for physical growth or a shrinkage of tuition-paying students?

While big-name endowment managers receive compensation well under 1% of the value of their respective universities’ endowments, Harvard claimed $1.8 billion in distributions that year with Yale making use of $1.3 billion from its returns. This somewhat (but not completely) vindicates the fact that their endowment managers are paid so well, but it can be also assumed that Harvard and Yale students would have appreciated a few more million dollars in financial aid on top of their sky-high cost of attendance sticker prices.

Dipping into Endowments

$35 billion is a lot of money for a non-profit. This is so much money that modern college endowments stimulated the creation of legislature like UMIFA and its successor, UPMIFA, the Uniform Prudent Management of Institutional Funds Act. These acts regulate how charitable donations to a not-for-profit organization can be invested and withdrawn.

We defined an endowment as the net value of a non-profit’s invested assets. Under UPFIMA, endowments are characterized by special restrictions that often prohibit the spending of the principal value gifted by a donor, prioritizing long-term yield and maximum, sustainable, and regular returns. Comparing this to a retirement account of sorts, we can now understand that endowments (under this code) serve as fixed-income portfolios to colleges and universities — allowing them to take out fractions of their capital gains tax-free.

Dealing with Inflation

So how do educational institutions know how much of their endowments to touch? In order to preserve the principal value of the endowment, one needs to take into account inflation and measures that decrease the purchasing power of the fund over time. FIRE investors use this principle when roughly determining the age at which they can retire with the 4% rule. If an endowment can expect a 10% return in one year, and people assume inflation will eat away at 2% of the purchasing power of the dollar in that year, then that college or university can, theoretically, spend up to 8% of their endowment in returns (or 80% of their returns) in that fiscal year.

Two things distort this example in the real world. Firstly, returns often average 7%, leading to a spending limit of 5% of the endowment per year. Secondly, college and university leaders desire to grow their endowments relative to inflation. All things accounted for, non-profit educational institutions typically spend 1-4% of their endowment’s value each year.

Implications for Students

Despite the fact that college and university endowments have been ballooning relative to inflation and the number of students attending said institutions, tuition continues to climb. In 1988, Harvard and Yales’ endowments were $4.1 and $2.1 billion. They are both at roughly nine times those values now. Tuition at those two schools increased from $11,645 and $18,060 in 1988 to $49,653 and $49,550 in 2017. During that same time, inflation only accrued 109%, roughly halving the purchasing power of the dollar. Instead of holding unused endowment returns culpable for their increases, tuition points its finger at the broad expansion of administrative personnel in college and university systems. Read more about “administrative bloat” here.

Institutions of higher education are moving to orient themselves as businesses in the twenty-first century. Massive endowment funds, high rankings on U.S. News and World Report, and jaw-dropping sticker prices all play to the allure of America’s most expensive colleges and universities. Public education systems aren’t immune to this predicament. College Board’s 2017 “Trends in College Pricing” report stated that the average cost of attendance (tuition, room and board, and other expenses) for an in-state public university was $25,890. With even subsidized education costing north of $100,000 for a four-year degree, college cannot be for everyone. However, public universities are following the lead of their wealthier private counterparts and beginning to offer more financial aid for socioeconomically disadvantaged students.

At the end of the day, remember that you don’t always get what you pay for. Large endowments don’t mean that beneficiaries like to use it to keep tuition costs stable (for economically advantaged students, at least). If you choose to look at endowment fund numbers, be sure to read reports of if and how management is spending returns and personally evaluate if their management is reasonable.