Intro

Gautam Adani was at one point the world’s second richest man with a net worth of $120 billion in August 2022; with a presence across multiple sectors, including transmission, generation, and airports. However, he now sits at $61 billion, half of what he used to be. With his listed companies taking a 42% hit in the past month, and nearly $80 billion worth of market cap being wiped across his companies, the questions remain: What exactly is causing this? Who are the people involved? And what is Adani doing to stop this?

The answer to these questions can all be related to one report from financial research & short selling firm Hindenburg Research, accusing the Adani family of fraud. Gautam Adani’s net worth has shot up by $100 billion in the past three years. This is mainly due to the insane levels of appreciation in Adani’s companies, with some such as Adani Gas increasing in valuation by almost 2021%. With such high growth, many became skeptical of how Adani achieved this. The key to this is found in the debt strategy the Adani companies used, and is also what Hindenburg locates as the point of initial fraud.

The Problem

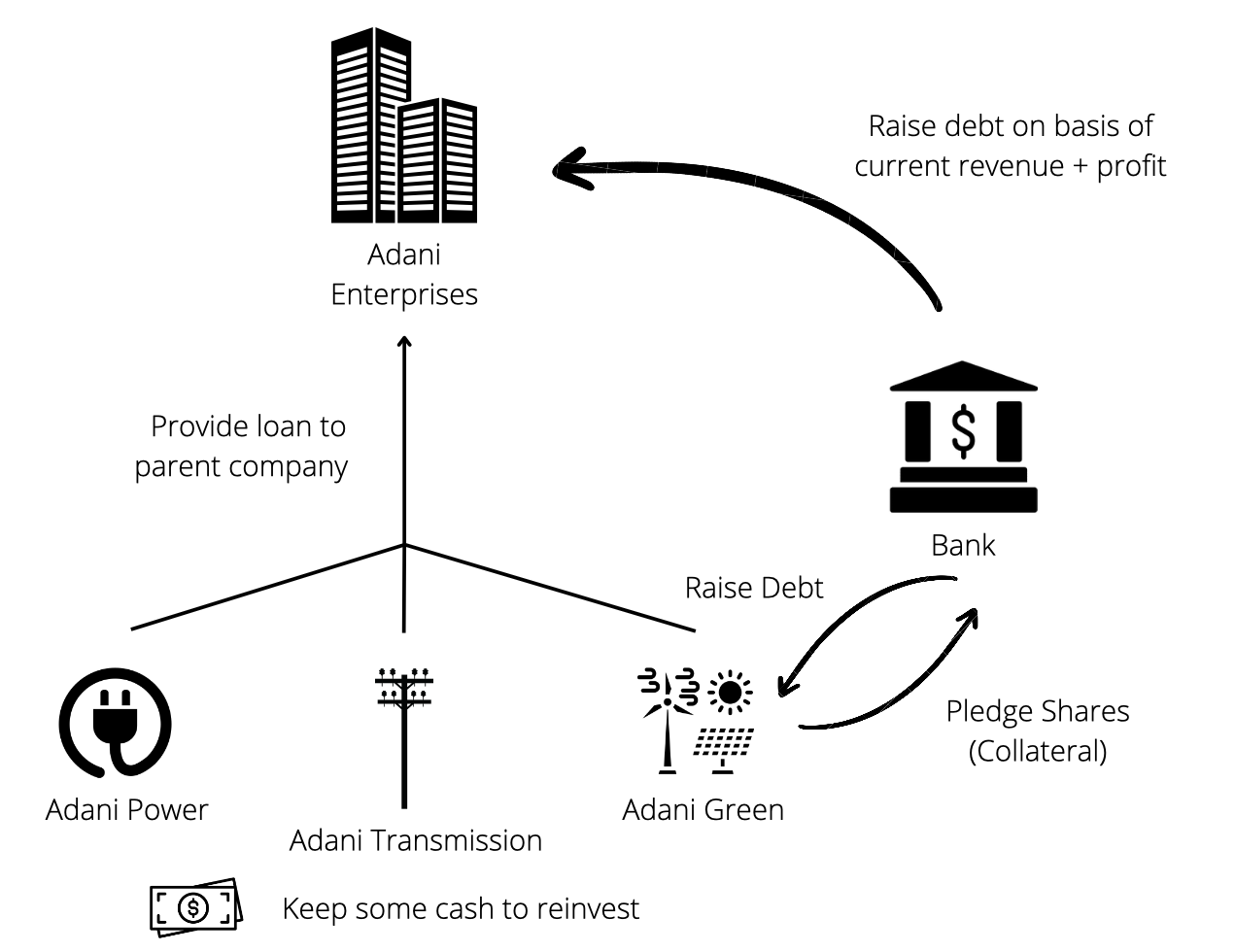

Adani currently has 7 listed companies, but this wasn’t always the case; until 2008, Adani had only 1 listed company, Adani Enterprises. Despite having a good reputation in the market, Adani enterprises struggled to raise debt when they got large contracts in the energy sector (Adani wasn’t operating in as many sectors at the time), as they still had relatively low levels of revenue and profit to take on loans of that caliber. To combat this, Adani made many of the subsidiaries of Adani enterprises public as daughter companies, and because the reputation of the Adani brand was already strong. The new IPOs were mostly hits. This allowed Adani’s companies to take advantage of share pledging, a means of using a company’s share equity as a means of collateral for a loan. This enabled Adani Enterprises to generate more cash-flow in a simple 3 step process. Firstly, Adani Enterprises (the parent company) would raise an initial amount of cash by borrowing at a low-cost without pledging any shares, but rather on the basis of their current revenue and profits. Next, they can get their daughter companies to pledge shares in order to collectively raise enough debt, which the daughter companies would then lend back to the parent company, while keeping some cash for their own growth.

This allowed the Adani group to engineer a cash-flow system which would create a cycle of positive growth wherein the debt they raised from banks would give them leverage to pick up large contracts in multiple sectors (e.g. airport operation of Mumbai), and then publicize this through the media, boosting investor confidence and further increasing Adani Group’s stock prices. When the stock price increases they can continue pledging more shares and hence raise even more debt to pick up even larger contracts.

However, this strategy is extremely risky; if the value of the collateral – the shares in this case – decreases, banks will have to take margin calls. In this case, they could ask the Adani group to top up the value of the collateral by selling their shares to provide more cash collateral. These margin calls could severely affect the share price of Adani’s companies, as when Adani dumps so many shares into the market at once for liquidity to provide to the bank as collateral, it will create an oversupply; prompting investors to panic sell and eventually causing the stock to crash. According to Hindenburg, in order to prevent this, Adani set-up shell companies in multiple countries including UAE, Mauritius and Cayman Islands, to ‘wash shares’ (considered a malpractice in every market), which essentially involves buying and selling the shares between these shell companies. What this can do is artificially increase demand and also show high trading volumes to investors, causing a rise in share price. Adani mostly did this to prevent banks from taking these margin calls when the value of his shares decreased.

Hindenburg Research’s Actions

Hindenburg claims Adani’s stocks have been overvalued for a long time with the PE ratio (a valuation metric which divides the price of the share by the dividend made of some of their companies) reaching over 400 (a 17 is considered overvalued in the US for reference). Moreover, Hindenburg commented there is “brazen stock manipulation” here and publicly challenges Adani Group. And Hindenburg really is putting its money where its mouth is, shorting Adani stocks, causing $10.3 billion of market cap to be wiped within one day.

Adani’s Response

Adani claims that he has no affiliation to these shell companies, despite the fact that the parent company of all of the shell companies (Monterosa Holdings) is owned by his niece’s family, and they can’t comment on the trading volumes and patterns of these companies. Moreover, Adani accuses Hindenburg of inciting a direct attack on not only him but also the growth vision of India, which has rallied a lot of support among Indian citizens.

Conclusion

Adani has always been key to India’s growth and has been front and center when it comes to India’s digital vision. Moreover, he has also been a close ally of PM Modi and has been a major supporter of his policies, many of which have landed him hefty government contracts. The whole of India including the top cabinet is watching, as if Adani goes down it will be a major problem for Modi, so it’s all hands on deck to help get Adani out of this.

Furthermore, India’s markets have a history of being shaken up by these scandals of high-net-worth individuals, whether it be the Harshad Mehta in the scam of 92 or the Ketan Parekh in the scam of 01. India’s growth has been powered a lot by foreign investment in recent years, with giants like Facebook partnering with Indian companies like Jio, but such activity in the markets will be deterred and growth is predicted to be stunted for Indian markets in the short-term for analysts. Despite this, the battle between Adani and Hindenburg is still far from over and how India will grow we will have to wait and watch.