If you walk up to somebody on the street and ask them to show you the contents of their wallet, they’ll probably give you a strange look and continue walking. But in the off chance that they agree to fulfill your suspicious request, you will probably find a few things in common within the wallets you see: probably some cash, a few coins, and a gift card here and there. If they’re over 18, you will likely also see a driver’s license and a few special pieces of plastic that are keys to their liquid financial assets. In other words, as a pickpocket, you would want to grab those little shiny things first and run. We’re referring to credit and debit cards here, which have different purposes despite the similar functions that they perform. But what’s the difference? What do they do? And should you get one?

The Difference Between Credit and Debit

Unless you have an exceptionally large wallet or a very secure place to store lots of cash, chances are you keep some (or most) of your money in a bank account. Banks turn your green paper into a number, giving us access to that balance through an account. One type of bank card — the debit card — charges a debit to your checking account whenever you make a purchase. This process is very direct: a business will check your bank account balance to make sure you have the funds to buy a sandwich, for example, before they give you the food you ordered. If your account balance is less than the cost of the sandwich, your purchase will be declined, and you will have to go hungry that night.

However, if you had a credit card, things would be different. Credit cards operate on the principle of credit (go figure), which means that a bank will trust you with a certain amount of their money — your credit limit. At the end of a specified amount of time (usually a month), the bank will ask you to pay them back for part or all of the money you’ve spent. Notice that you can pay part of that balance. Credit cards let you give a minimum payment, in which case you run a balance: carrying some of your debt to the bank from one payment period to the next. With a debit card, you could never do this because you cannot spend money that isn’t present in your account.

That Piece of Plastic Has Rules

The limits of each type of card are relatively logical. Because using a debit card is like spending digital cash, you can’t overdraft your account (spend more than you have), which limits what somebody malicious could do if they got their hands on your card information. Daily spending limits and ATM cash withdrawal limits ensure damage control and help cardholders cap spending. Additionally, debit cards generally require a PIN when making a purchase, adding a level of security not typically found on credit cards.

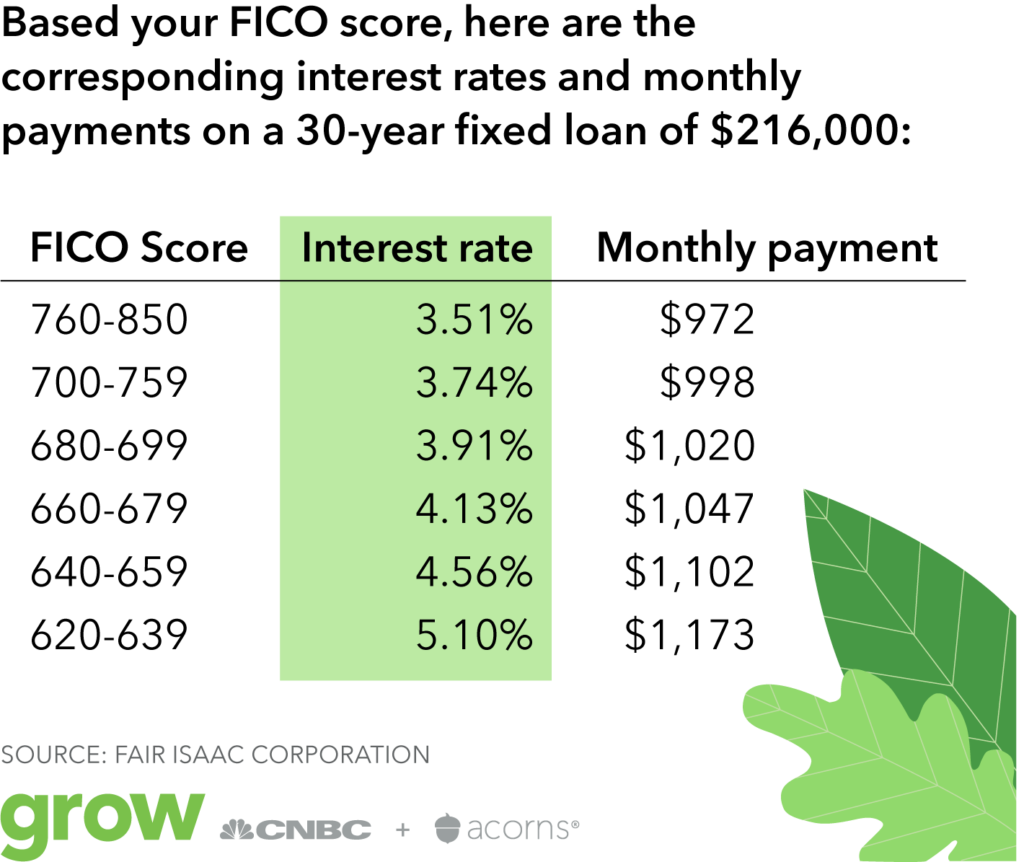

Credit works a bit differently. Because a credit card isn’t tied to an account with money in it, you can become indebted to the bank by running a balance. When you make payments less than your full balance, a bank will charge interest on the amount you owe to them month after month. These interest rates can be ridiculously high — in the neighborhood of 15+% APR (annual percentage rate). Read about why this matters here. For reference, home mortgages typically fall in a range around 5% APR, and personal loans run into the teens. Like all debt, it’s best to avoid credit card debt at all costs.

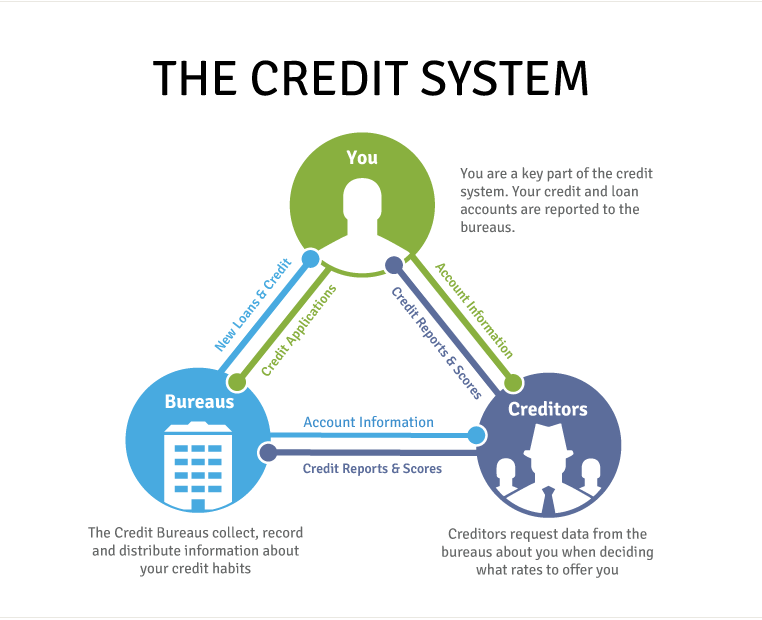

Credit Scores

When you go to take out a loan like the ones mentioned above, a bank will usually ask for your credit score, which indicates how trustworthy you are with other peoples’ money. This number is calculated from how you use credit: paying back loans to lenders, whether they be on a credit card or through a home mortgage. There are tons of factors that can influence your score, like length of time using credit, credit utilization (how much of your limit you spend each month), and if you pay on time and in full — the last part being the most important. You can read more about credit and scoring systems here. Basically, maintaining a good credit score is essential for the average person in a developed economy to have financial freedom.

Deciding Which To Use

At the end of the day, debit and credit cards have different purposes. If you have a bank account and want to spend money within that account, you definitely should have a debit card. Unless you like carrying around cash everywhere you go, which is more prone to theft and untraceable if stolen, the choice to go debit is clear. Getting one is easy: all you typically have to do is ask for one if you have an existing account with a bank or credit union. While checking accounts may have an associated monthly fee if certain criteria (i.e. minimum spending per month, age of account holder) are not met, most financial institutions offer cards with special spending and withdrawal limits for teenagers, lowering the barrier to access further.

Credit cards are a different story. While there are obvious liabilities associated with carrying a credit card — no PIN, spending money that isn’t yours, and the consequences of running a balance — getting one is the first step towards building a credit score, which is necessary in an economy like America’s. A bank will have you fill out an application for a card and then approve or deny it based on your age, past credit history, and employment status. For reasons of responsibility for debt, only gainfully employed adults are typically granted credit cards by banks. Yes, financial institutions can profit off of people who choose not to make full payments every month, but those institutions also want to ensure that those people will eventually pay off their cards. Credit cards are money makers for banks, so you want to be careful how you use them.

Credit Cards And Discounts

However, there are a few big pluses to using a credit card the right way. You may be able to access sizable discounts from department stores that offer credit lines for shopping within their store, also known as rewards cards. People make use of credit rewards through a technique called churning, or opening new credit cards to take advantage of discounts and benefits and then closing those cards once they’re paid off. This can be a good idea if you can keep track of lots of cards and can remember to pay them all off. Churning can be bad for your credit score, though, so it’s a good idea to limit the number of cards you open every year.

“Credit and Debit,” Not “Credit or Debit”

Instead of thinking about whether you need a credit card or a debit card, you should think about if you need each of them. Almost everybody with a checking account can benefit from a debit card, but not everybody who is eligible for a credit card should get one. Debit cards are essentially digital replacements for cash that’s already yours. On the flip side, credit cards are designed to take advantage of our impulse to spend others’ money as if it isn’t our own. If you’re wise with credit, you can get access to rewards and loans much easier, not to mention lower interest rates on those loans. But if you screw up on your payments or put a dent in your score, you’ll be better off never having applied for a credit card in the first place.