Many financial enthusiasts have most likely heard of the film The Big Short, adapted from the book by Michael Lewis with the same title. The story follows one of the greatest trades in Wall Street history where a hedge fund manager, Michael Burry, from California predicted the financial crisis of 2008 and made his investors $700 million over the time span of 2 years.

Michael Burry was able to do so by buying credit default swaps (CDS), a financial swap agreement where the seller of the CDS agrees to pay the buyer in the event that the debt defaults. It’s basically buying insurance on an asset default. This “insurance” can be cheap or expensive based on the market’s perception of the risk of default. The CDS premium is what the buyer of a CDS pays to the seller in order to receive the protection and payout in case of a default. In other words, that premium is the cost of insuring against a bond default in a given time period.

Recently, another big investor made headlines for his “Big Short” through his purchase of credit default swaps. Bill Ackman turned a $27 million investment in CDSs into $2.7 billion in a matter of 30 days, leading some people to refer to it as the greatest trade ever.

Introduction to Bill Ackman

Bill Ackman is the founder and manager of Pershing Square Capital Management, a hedge fund based in New York City. The hedge fund has around $8 billion under management as of June 30, 2019. You may know him for his famous battle against Herbalife, where he took a huge short position due to his conviction that the company is a pyramid scheme. You may also know Ackman for his famous activist moves in companies like Canadian Pacific Railway, Wendy’s, and JCPenney. Bill Ackman is widely known as a great investor on Wall Street. He has outperformed the market by over 600% between 2004-2020.

The Trade

How did Bill Ackman turn $27 million to $2.7 billion in only 30 days? The answer is COVID and its effect on corporate debt. Ackman predicted that attempts by the US government to contain COVID will have a huge negative effect on US markets. Ackman worried about the effect of the virus so much that he considered liquidating all of his assets into cash. However, he decided that it would be better to protect his assets by buying CDS on corporate bonds. This would insure his firm’s positions in the event of negative market movement.

Ackman bought credit default swaps where he would have to pay $27 million every month for 5 years (5 years is the usual limit for a CDS contract) until he sells his position and makes a profit or the time expires. This meant that Ackman would have to pay $324 million a year in premiums. The credit default premium rate was 0.5% on corporate bonds before COVID caused a spread widening.

By dividing $324 million in monthly premiums for a year by the 0.5% CD insurance rate, you will get $64.8 billion worth of bonds that Ackman was buying protection on. The notional amount is the amount of bonds you protect yourself against. The entire US market has $6 trillion in investment-grade bonds. This means Ackman was essentially buying protection on around 1% of all corporate bonds in the market.

Why Use Credit Default Swaps

Why would someone buy a credit default swap? Credit default swaps are much safer because losses are limited compared to the possibility of infinite losses when shorting bonds or stocks.

One example is a house that you bet will burn down so you buy fire insurance on it. You will have to pay monthly fees on the insurance contract until the house burns down or until the contract time expires. If the house does not burn down during that time period, then you only lose the limited amount of money that you paid on the insurance contracts over that time period. If you directly shorted the house with the hopes of it burning down, then the amounts of money you could lose are unlimited. This is basically the case with the CDS (fire insurance) and the corporate bonds (house). By buying credit default swaps, Ackman could limit his losses to about $1.56 billion in the worst case scenario.

Ultimately, the best way to think about a CDS is insurance against a bond defaulting. If nothing goes wrong, then you lose what you pay in premiums. If the bond defaults, then you get a payout.

CDS Premiums and Spreads

CDS prices are known as premiums or spreads and are represented in basis points (bp). 1 basis point is equivalent to 0.01%. This percentage is representative of the amount needed in order to protect against defaults of a company. An example to highlight the relationship between basis points and the CDS premium is as follows. Company A has a spread of 300 bp. The insurance rate would be 1/100 of 300 bp, which is 3%. This means that in order to protect against $100 worth of debt for company A, the investor would have to pay a fee of $3. This is important to understand when it comes to Ackman’s trade and where the values below are derived from.

Effect on Credit Spreads

COVID caused pessimistic market outlooks on a very grand scale. Due to this, the effect on credit spreads was very significant. Credit spreads are the difference in yields of corporate bonds and the yield of secure Treasury bonds. Treasury bonds are bonds issued by the government, which provides a guaranteed yield over a 10-30 year period. The risk is very low on these Treasury bonds while the interest rate is also very low. The Treasury bond’s interest rate constantly changes but is always lower than corporate bonds. Corporate bonds have a much higher interest rate due to the fact that investors are taking a much higher risk. Corporate bonds do not have the same creditworthiness on their obligation as Treasury bonds do.

COVID has many investors worried about increased credit risk due to the virus’s large scale effect on many industries. Credit worthiness is severely lowered due to the increased risk. Investors sold many corporate bonds, causing a decrease in prices and an increase in yields in the corporate bond market. They bought into secure Treasury bonds as they are safe, causing an increase in prices and a decrease in yields in the Treasury bond market. This causes the credit spreads to widen as there are higher yields on the corporate bonds and lower yields on the government bonds.

Why Credit Spreads Matter

Tightening credit spreads are an indicator that corporate creditworthiness is increasing, which is an indication of a healthy economic environment. Widening credit spreads indicate that investors believe companies will have trouble paying back their debts, which is an indication of unhealthy business conditions. Widening credit spreads also makes CDSs more valuable. This is because you can sell and make the difference from the original spread subtracted from the wider spread. In Ackman’s case, the credit spreads widened about 3 times, leading Ackman to a huge profit on his initial trade.

CDS Valuation

CDS valuation is as simple as understanding the present value and future value. The present value of a CDS is simply the total amount that would be paid in premiums over the CDS’s duration when the investor first purchases the contracts. When credit spreads widen or tighten, the price of CDS contracts, represented by the CDS premium (the “insurance rate”), increases or decreases respectively. The total premium amount of the CDS duration also rises or falls as credit spreads widen or tighten. That total amount paid is the future value. It is always constant as the payments are a fixed amount per time period and for a set duration. This means that the owner of that CDS can sell it for a profit or a loss depending on the situation.

If there is a profit, as in Ackman’s case, the profit is equal to the present value of the CDS’s total cost over its duration after credit spreads widen minus the CDS’s total cost over its duration at the spread you originally bought it at. The exact same math applies to losses, but, instead of widening, credit spreads tighten and cause the future value to be lower than the present value. The investor would then have to sell at a loss or can keep his position until the duration of the contract. This makes perfect sense — as the risk of corporate defaults increases, the cost of protecting yourself against them also increases, leading to a higher value for the CDS protection in the market.

Steps for CDS Valuation

The steps laid out below simplify the valuation and potential profit of a CDS.

- Find the present values of the CDS’s monthly premiums and sum them up. This is the present value of the entire CDS before credit spreads change. The initial credit spread multiplied by the notional amount determine the monthly premiums.

- After credit spreads change, find the present values of the CDS’s monthly premiums and sum them up. This is the present value of the CDS after credit spreads change.

- Subtract the present value of the CDS after credit spreads changed from the present value of the original CDS. This becomes your profit or loss.

If spreads have widened, then your profit should be positive as the CDS’s present value after credit spreads widen are higher. If spreads have tightened, then your profit should be negative as the CDS’s present value after credit spreads tighten are lower. This is essentially how investors make profits or losses off of CDS contracts.

The Profit

As established earlier, Ackman would have had to pay $27 million over 12 months for a total of 5 years. This would amount to $1.62 billion in total premiums paid if he had held on for 5 years. The total amount of $1.62 billion would have been discounted to about $1.56 billion as the treasury rate was 1.5% for 30-year Treasury bonds. The 30-year Treasury bond is considered here instead of the 5-year Treasury bond as it offered a higher yield due to the longer time span it was set for. If an investor wanted to find the option that yielded the highest return without any risk, then the 30-year Treasury at the bond would be what they invest in. Treasury bonds are considered risk-free because they are backed by the US government, which is widely believed to never be able to default.

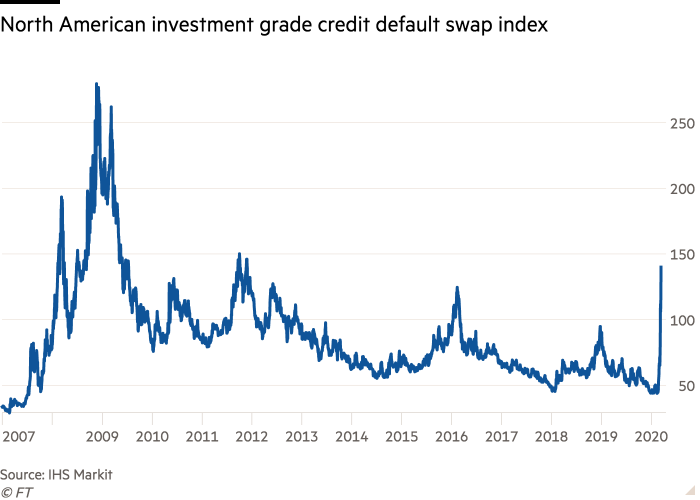

When he entered into this CDS contract, $27 million per month represented a 50 bp spread on the notional amount of $64.8 billion. Essentially, he needed to pay 0.5% of the notional amount he was receiving protection against per year for 5 years. Credit spreads were also at 0.5%, so the CDS contract premiums are more or less equal to the prevailing credit spreads for the bonds being protected against. But, he bet on credit spreads widening as a result of COVID damaging corporate creditworthiness, thus negatively affecting corporate bonds. He was right as credit spreads on the corporate bond index increased from 0.5% to 1.35% or 50 bp to 135 bp.

Ackman’s CDS Valuation

Applying the numbers from Ackman’s trade to the CDS valuation we laid out can help us understand his large profit.

- 50 bp x $64.8 billion x 5 = $1.620 billion. Total amount paid on the CDS before spreads widened is $1.620 billion.

- Discount the old premium of $27 million by the monthly discount rates. Then, add up all 60 months of the different monthly premiums to get the discounted value (look here for specifics). This amounts to about $1.56 billion.

- 135 bp x $64.8 billion x 5 years = $4.37 billion. Total cost of CDS contract after spreads widened to 135 bp from 50 bp is $4.37 billion.

- Discount the new monthly premium of $72.9 million by the monthly discount rates. Then add up all 60 months of the different monthly premiums to get the discounted value (look here for specifics). This amounts to about $4.2 billion. Ackman received this amount by whoever he sold the CDS to.

- Subtract them: $4.2 billion – $1.56 billion = $2.64 billion

- Ackman’s profit is about $2.64 billion

The values are not exact in the steps. More specific values on the spreadsheet, so profit number differs on the spreadsheet.

Discounting

The way to find the monthly discount rates is simple. Since the discount rate is the risk-free rate at the time — 1.5% per year — all that you need to do is find out how much of that has been applied in what month. So for the 1st month, only a twelfth of the 1.5%, or 0.125%, is applied. So the discount rate for month 1 is 1.00125. For the 2nd month, only a sixth of the 1.5% is applied, or 0.25%. Hence, the discount rate for month 2 is 1.0025. This continues all the way to month 60, where the discount rate would be 1.075. This is because 1.5% per year is 7.5% overall growth over 5 years due to simple interest that bonds pay.

Ackman exited his position at the peak basis point of about 135-140 bp on March 23, 2020. This was when CDS contracts were at their peak in terms of basis points. Full calculations are on this spreadsheet: Ackman Trade CDS Profit. Only Ackman and Pershing Square know the exact figures regarding the trade. The values above are valuations that are based upon approximations using publicly available information rather than exact numbers.

The Controversy

As usual, big trades with big profits usually create some sort of controversy or complaints from the public. In Ackman’s case, the controversy was that Ackman went on CNBC and called for a shutdown of the economy. People thought that the shutdown would significantly help Ackman’s position in the CDS trade. People thought he was yelling fire in order to cause the stock market to go down and make a profit. What people may not know is that Ackman already exited half of his position by the time he went on CNBC calling for a shutdown. This implies that the market was already down and Ackman was just giving a warning from whatever may come next.